The FIDA Discussion: Opportunity or Setback for the Future of European Finance?

Recently, there has been an uproar in the financial world surrounding the Financial Data Access (FIDA) regulation – an initiative that was supposed to shape the future of the European financial landscape in a sustainable way. As the CEO of a company operating at the intersection of traditional finance and digital innovation, I would like to share my perspective on the recent developments.

The FIDA Rollercoaster

The past weeks have been like a real rollercoaster ride: First, news circulated that the EU Commission intended to completely withdraw the FIDA regulation, then rumors followed about a possible 180-degree turn. Currently, however, everything indicates that the project will continue for the time being. FIDA was still listed as a “pending proposal” in the Commission’s 2025 work paper published on February 12, 2025. A development that I fundamentally welcome.

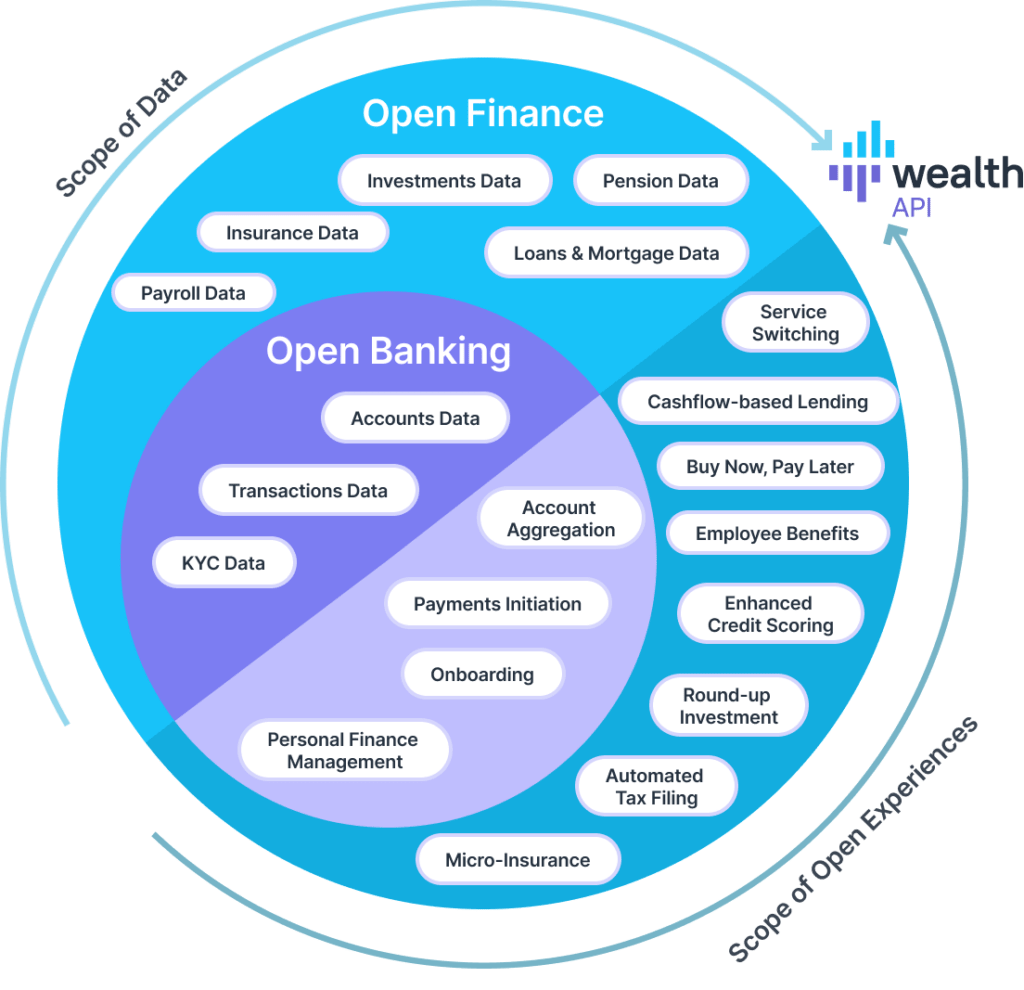

The original idea behind FIDA is clear and forward-looking: The PSD2 reform (open banking for payment accounts) is to be extended to all financial services. This would mean that third-party providers could access not only account data, but also customer data from investment products, portfolios, and loans. Of course, always with the customer’s consent. Unlike PSD2, financial institutions such as banks should be allowed to charge for providing this data, which I consider a sensible approach.

Between Lobbyism and Legitimate Concerns

Criticism of FIDA came primarily from the insurance industry and partly from the banking sector. This reaction is understandable, as any opening of data silos means change and potential new competitors. Especially for insurance companies, FIDA would be a paradigm shift, as they have not yet been confronted with “open finance” requirements.

However, the original FIDA proposal did have weaknesses that would have led to unnecessary bureaucracy and burdens for companies. According to many stakeholders, the complexity and implementation costs were disproportionate to the perceived benefits for customers.

The Danger of a Missed Opportunity

A complete withdrawal of FIDA – or even just a years-long delay – would be a significant setback for the digital transformation of European finance. As a company that develops digital interfaces for asset managers, we experience the challenges of the status quo daily: Without uniform standards, we have to build separate interfaces for each individual bank. An enormous effort that slows down innovation and scaling.

Today’s asset landscape is fragmented. Customers maintain multiple banking relationships, their assets are distributed across various custodians, and specialized service providers offer different services. Without standardized data access, it becomes increasingly difficult to provide customers with a holistic overview of their financial situation and to offer tailored solutions based on that.

Lessons learned from PSD2

The implementation of PSD2 has shown that well-intentioned regulation can miss its mark through over-regulation. A concrete example from our practice: The need for two-factor authentication for transaction data older than three months poses an unnecessary hurdle for users. Such details may seem small but have massive impacts on usability and thus on the success of the entire initiative.

The better approach would be for the EU to define clear goals: such as reducing fraud cases to a certain percentage. It should then leave it to companies to decide how to achieve these goals. This approach would promote innovation instead of stifling it with rigid requirements.

International Competition Is Not Waiting

While Europe debates, other regions are acting. We are in a global competition for the best financial solutions, and every delay costs us ground. Especially for European FinTechs, the lack of standardized data access becomes a growth inhibitor. Missing standards lead to complex and costly individual developments that can stifle innovative business models in their infancy.

The Future of Wealth Management Needs Open Finance

In a time when we can unlock completely new possibilities for wealth management through artificial intelligence and machine learning, access to comprehensive data is the key to success. A data-driven wealth management, as we strive for at wealthAPI, enables:

- Individual investment strategies, precisely tailored to each customer’s goals and risk tolerance

- Automation of routine tasks, allowing advisors to focus on value-added activities

- Transparent decision-making, where customers have insight into their investments at all times

- Scalability, to ensure high quality standards even with increasing customer numbers

All these benefits can only be fully realized if we have simple, standardized access to all relevant financial data. Exactly what FIDA was supposed to enable.

The Way Forward

The current situation also offers an opportunity: We can learn from the discussions and criticisms and develop an improved FIDA proposal that takes into account the legitimate concerns without losing sight of the fundamental goal.

As an entrepreneur, I am ready to actively participate in shaping such an optimized proposal. We need a framework that promotes innovation while ensuring the protection of customer data and avoiding unnecessary bureaucracy.

I expect three things from the EU Commission:

- Determination: A clear commitment to the basic idea of open finance.

- Pragmatism: The willingness to learn from the mistakes of PSD2 and avoid superfluous regulation.

- Speed: An ambitious timetable to avoid falling behind other regions.

The democratization of wealth management, i.e., high-quality financial advice for everyone and not just for the wealthy, will only succeed with an open data landscape. FIDA could create the decisive framework for this.

A Future-Oriented Outlook on Europe’s Financial Landscape

The current discussion about FIDA is more than just a technical regulatory debate. It is about the fundamental question of how we position European finance for the digital future. A complete departure from the open finance principles would be a serious strategic mistake.

As a technology provider at the intersection of traditional wealth management and digital innovation, we see daily the potential that lies in an intelligent linking of financial data. Realizing this potential – for the benefit of consumers and to strengthen the European financial center – should be our common goal.

The future of wealth management will be hybrid: the perfect balance between human expertise and technological innovation. To make this vision a reality, we need a smart, balanced regulatory framework for access to financial data. Nothing less, but also nothing more.

wealthAPI Blog

wealthAPI Featured in Bitkom White Paper: Compliance Automation as a Real-World Use Case

In March 2026, the German digital association Bitkom published the white paper "Beyond the Pilot –…

Wealth Aggregation as the Foundation for Personalized Advisory: wealthAPI in the Fincite WealthTech Radar 2026

Susanne Krehl, Chief Growth Officer at wealthAPI, contributed a guest chapter on Wealth Aggregation…

wealthAPI Appoints Nicola Breyer as Open Finance Expert to Advisory Board

Berlin, February 10th, 2026 - wealthAPI, the leading provider of data and API solutions for the…